First, the overview of the auto parts industry

01 Basic introduction of auto parts industry

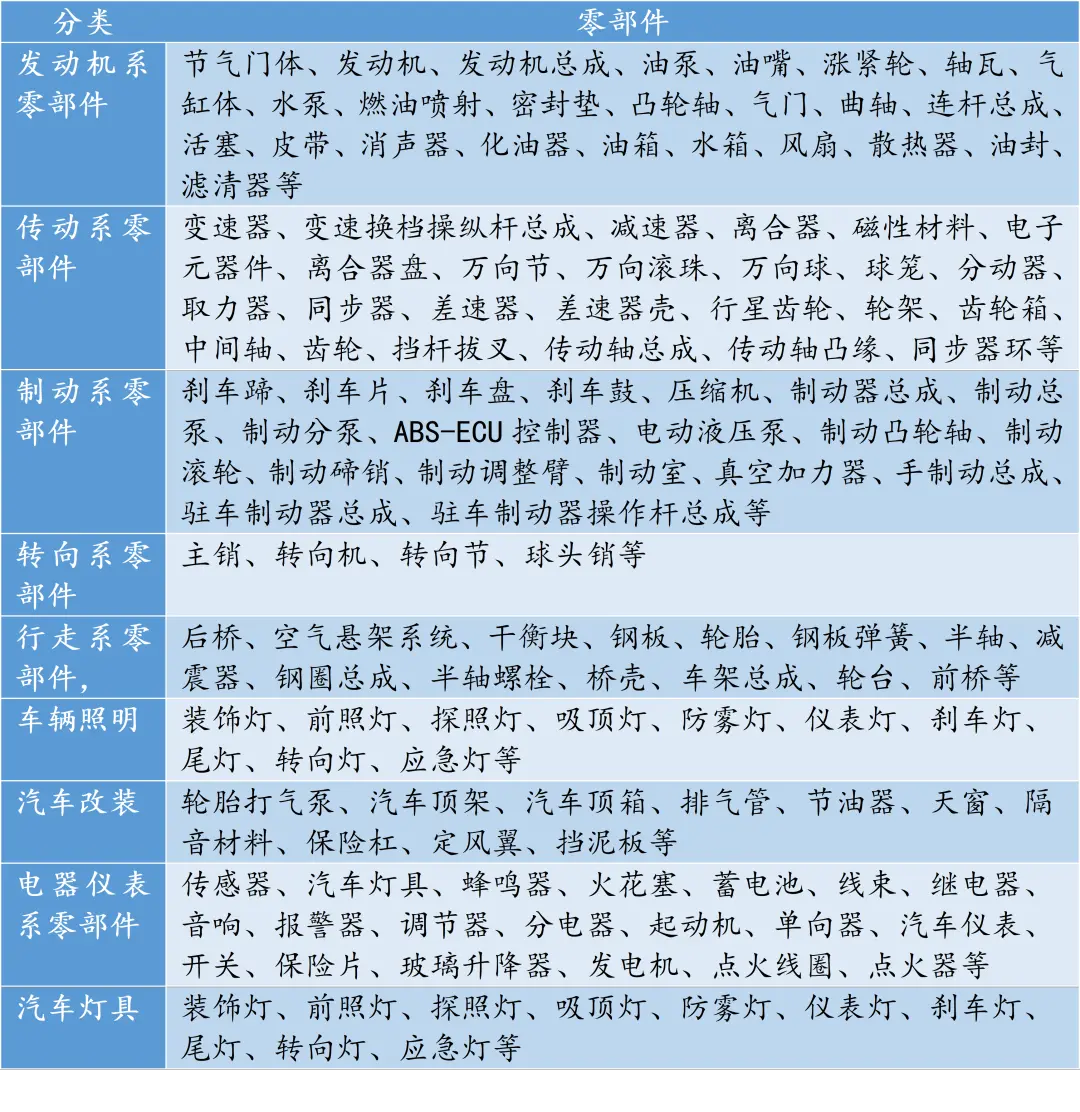

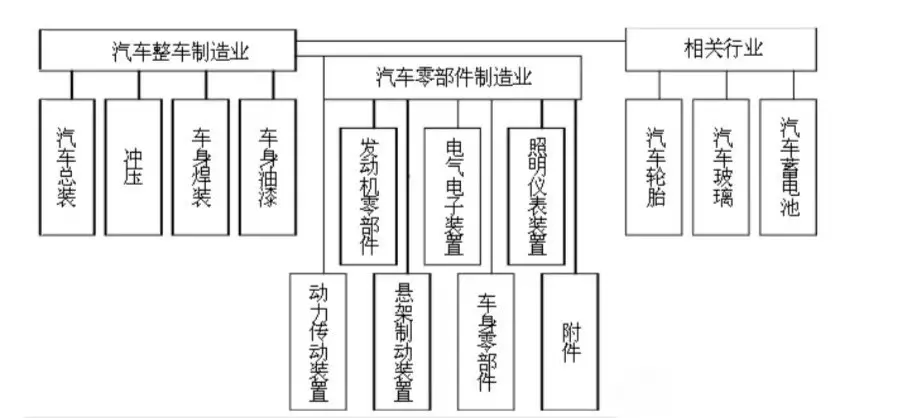

Auto parts are various spare parts of motor vehicles and their bodies. Automobiles are generally composed of four basic parts: engine, chassis, body and electrical equipment, so various subdivided products of auto parts are derived from these four basic parts. According to the nature of the parts, it can be divided into engine system, power system, transmission system, suspension system, brake system, electrical system and other (general supplies, loading tools, etc.).

List of major products for auto parts

In 2021, China's automobile production and sales will reach 2608.2 million units and 2627.5 million units, respectively, a year-on-year increase of 3.4% and 3.8%, ending a three-year consecutive downward trend. New energy vehicle sales reached 3.352 million units, a year-on-year increase of 1.1 times, ranking first in the world for seven consecutive years.

02Auto parts industry chain

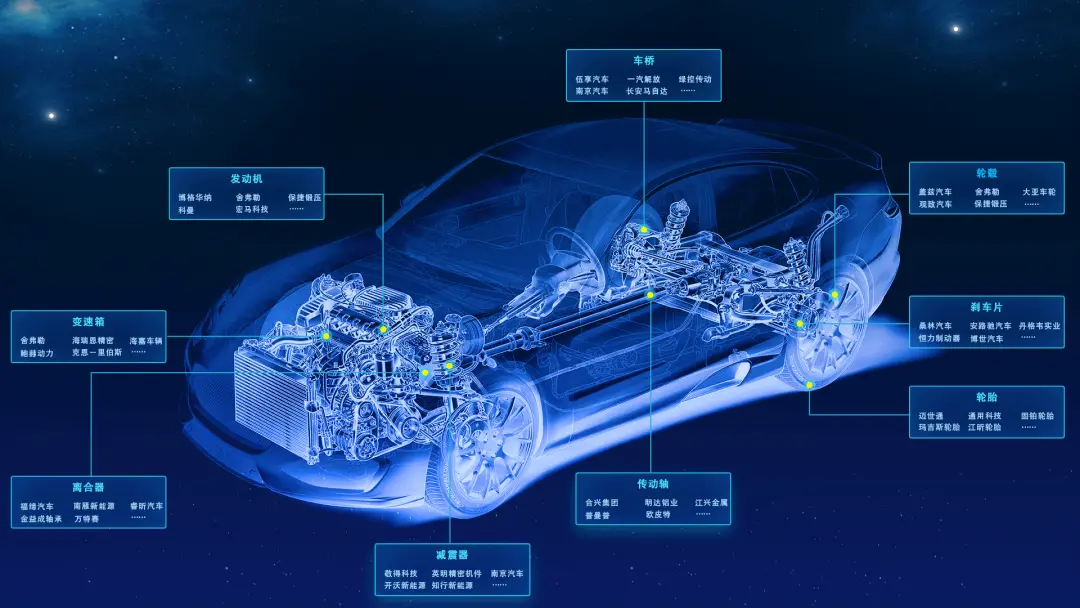

The upstream of the industrial chain of auto parts is raw materials and design, among which the demand for raw materials is steel, non-ferrous metals, electronic components, plastics, rubber, and glass. Downstream are vehicle manufacturers and service maintenance organizations, including automobile manufacturers, automobile 4S shops, automobile repair shops, auto parts suppliers and automobile modification factories.

From the perspective of the upstream industry, the price of raw materials for the production of parts and components industry is mainly determined by the market price of bulk commodities such as steel, petroleum and natural rubber. In recent years, due to the frequent fluctuations in the prices of iron ore, petroleum, natural rubber and other resource commodities, the prices of steel, rubber, plastics and other chemical materials have also fluctuated sharply, which has caused certain pressure on the stability of production and operation of the domestic auto parts industry.

From the perspective of the midstream industry, China's auto parts industry after years of development, product development, processing technology, quality control and after-sales service have made great development, has formed a set of relatively complete auto parts supporting supply system and important enterprises, favorably supported the improvement of the domestic auto industry system, laid an important foundation for the development of domestic independent brands. The automotive electronic control system industry is an important midstream industry in the entire automotive industry system, carrying nickel-metal hydride and lithium battery related battery material industries in the upstream and connecting the automotive product industry downstream. It consists of three main modules: battery module, motor and control module, and vehicle control module. Among them, the battery module includes two parts: power battery and battery management system; The motor and control module include two parts: frequency conversion speed control controller and drive motor; The vehicle control module includes two parts: CAN bus and vehicle control system.

From the perspective of the downstream industry, benefiting from the development of the vehicle industry at home and abroad and the expansion of the consumer market, the domestic auto parts industry has shown a good development trend. The downstream customers of domestic parts suppliers are mainly domestic and foreign vehicle manufacturers and their parts suppliers, and the customer concentration is relatively high, so parts companies are in a relatively weak position in negotiations with downstream customers. However, for some parts suppliers with leading advantages in a certain market segment, their market position and technical advantages will help to enhance market discourse power and bargaining power, so they have a certain ability to transfer costs downstream.

Second, the development status of the auto parts industry

01National policies support the development of auto parts

As a sub-industry of the automobile manufacturing industry, auto parts and accessories manufacturing is the basis for the development of the automobile industry. As an important pillar industry of China's national economy, the automobile industry has received strong support from the state. With the rapid development of the industry, the State Council, the National Development and Reform Commission, the Ministry of Industry and Information Technology and other relevant departments have issued a series of policies and regulations to standardize the development of the industry and guide industrial transformation and upgrading.

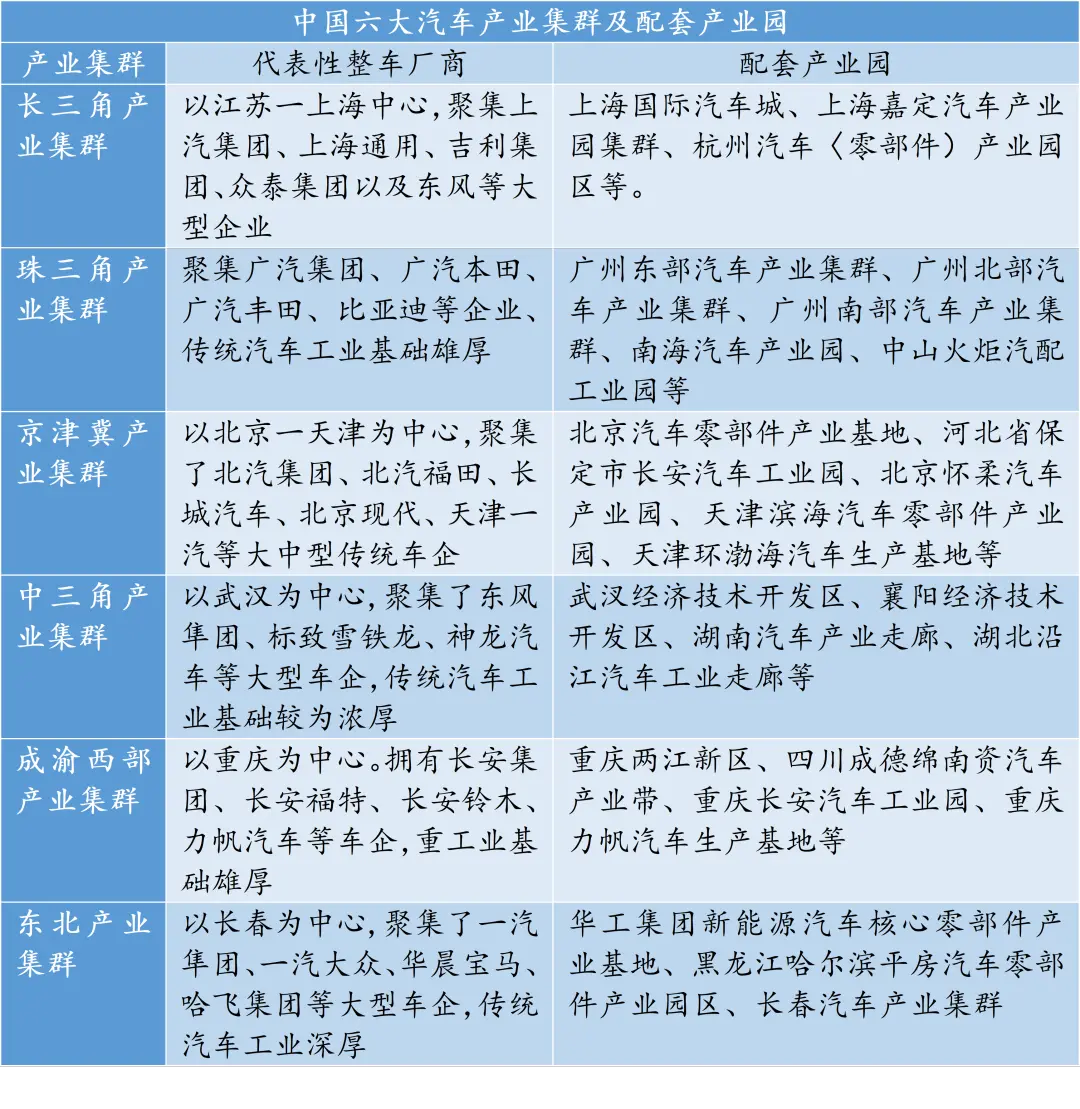

02Auto parts form six major industrial clusters

With the rapid development of China's automobile industry, six major automobile industry agglomeration areas have been formed in China, which are in the Yangtze River Delta cluster, the Pearl River Delta cluster, the Beijing-Tianjin-Hebei cluster, the Middle River Delta cluster, the western cluster of Chengdu and Chongqing, and the northeast cluster. Auto parts manufacturing enterprises usually build around vehicle manufacturers, forming six major industrial clusters, mainly including the Yangtze River Delta industrial cluster with Shanghai, Jiangsu Province and Zhejiang Province as the core, the western Chengdu-Chongqing industrial cluster with Chongqing and Sichuan Province as the core, the Pearl River Delta industrial cluster with Guangdong as the core, the Northeast industrial cluster with Jilin, Liaoning Province and Heilongjiang Province as the core, the Central Delta industrial cluster with Hubei Province, Hunan Province and Anhui Province as the core, and the Beijing-Tianjin-Hebei industrial cluster with Beijing, Tianjin and Hebei Province as the core.

03The sales revenue of auto parts continues to expand

With the rapid development of China's automotive industry, the increase in car ownership and the expansion of the auto parts market, China's auto parts industry has developed rapidly, and the growth rate is higher than that of China's vehicle industry.

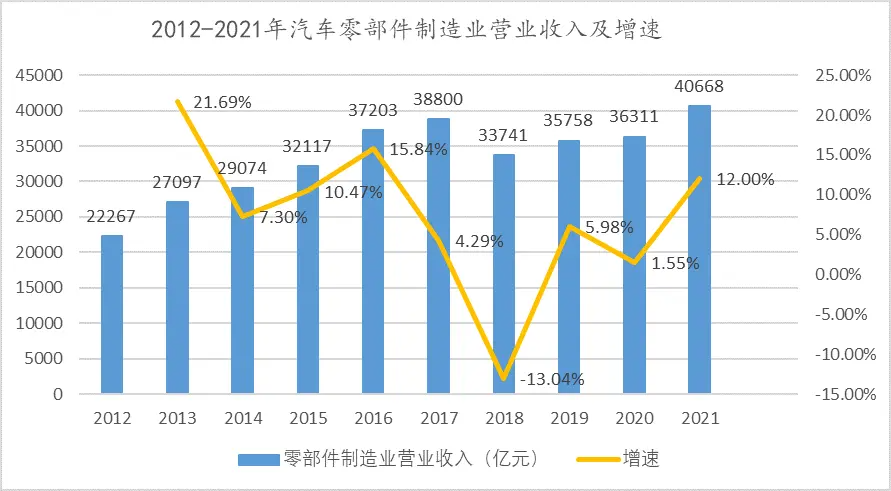

With the vigorous development of China's automobile industry, domestic brand auto parts enterprises almost cover the vast majority of auto parts fields. With the continuous improvement of the domestic auto parts manufacturing level and the development of new energy vehicles, the auto parts industry has also developed rapidly. According to the data of the National Bureau of Statistics, from 2012 to 2021, the proportion of the output value of China's auto parts manufacturing industry in the total output value of the automobile industry has basically remained above 40%.

Affected by industrial policy adjustments and domestic substitution, the income of China's auto parts manufacturing enterprises maintained a steady growth trend from 2014 to 2017, and since 2018, China's auto industry has entered a development platform period, and the overall production and sales scale has declined compared with 2017, and the revenue scale of China's auto parts manufacturing enterprises in 2021 will be 40,668.12 billion yuan, a year-on-year increase of <>%.

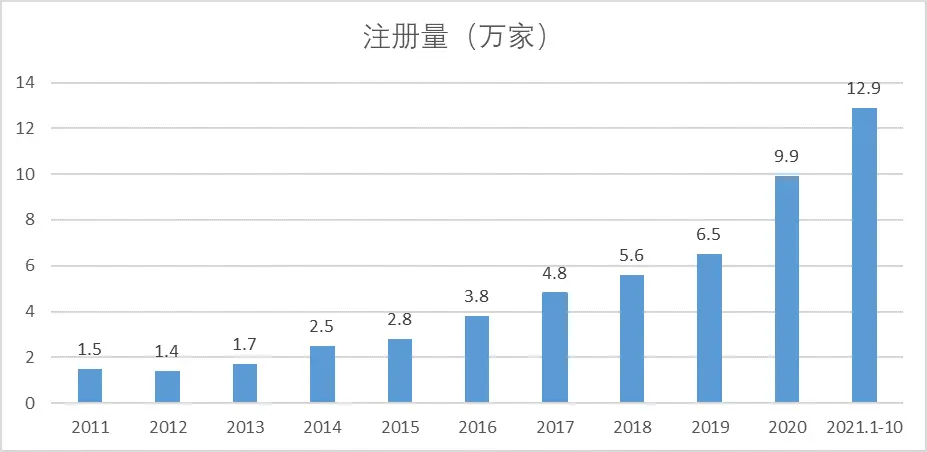

04The number of auto parts registrations increased

In the past ten years, the number of auto parts-related enterprises has been increasing year by year. 2020 was the peak period for enterprise registration, with 9,9 annual registrations, a year-on-year increase of 52.7%. In the first 2021 months of 10, a total of 12,9 auto parts-related companies were newly registered, a year-on-year increase of 76.7%.

05Excellent auto parts enterprises have emerged in large numbers

In 2022, the number of Chinese auto parts companies on the list of the world's top 2012 auto parts companies has gradually increased, from only 1 company on the list in 2022 to a total of 11 companies on the list in <>. Chinese enterprises ranked among the world's top <> mainly rely on the advantages of traditional segments (such as the commercial vehicle market) and frontier fields (such as new energy), and their revenue growth rate is higher than that of foreign-funded enterprises.

Third, the development trend of auto parts industry

01Auto parts manufacturers are gradually showing a trend of collectivization

The auto parts industry plays an important role in the automotive industry chain. According to the "China Auto Parts Industry Development Report" jointly compiled by the China Association of Automobile Manufacturers and the China Automotive Engineering Research Institute, there were more than 2018,10 auto parts companies in China in 2, of which 000,1 had sales revenue of more than 3 million yuan, and their products basically covered nearly 1,500 parts in the automotive industry chain. In recent years, China's economy has shifted from high-speed growth to high-quality development, with the continuous improvement of domestic automobile ownership, as a large country in automobile production and sales, China's automobile industry has also entered a new stage of high-quality development, auto parts manufacturers gradually show a trend of collectivization, a small number of leading enterprises with their own competitive advantages monopoly part of the production of parts, and provide a number of vehicle enterprises.

02Modular supply brings greater development opportunities to auto parts enterprises

Modular supply refers to the mode of supplying parts suppliers to the main engine factory not with a single part, but in the form of the entire system module, involving modular product design, modular production and modular procurement. Under the modular supply mode, OEMs can make full use of the innovation, development and testing advantages of parts and components enterprises, and transfer most of the design tasks to parts enterprises, so as to optimize the vehicle production process, reduce vehicle manufacturing costs, and accelerate the iteration of new models by shortening the design and development process of the whole vehicle. Auto parts enterprises undertake more new products and new technology development work under the modular supply mode, intervene earlier and more deeply in the design, research and development, and production process of the whole vehicle, provide professional suggestions for the development of new models at the early stage of design, and actively cooperate with the main engine factory for supporting development. In this process, OEMs are increasingly dependent on parts and components companies in terms of products and technologies, and parts companies gradually form and master the core technologies of product design and production in the development process, and play an increasingly important role in the automotive industry chain.

03Localization of auto parts procurement

With the increasingly fierce competition in the automobile manufacturing industry, and the gradual saturation of the automobile consumer market in developed countries and regions such as the United States, Europe and Japan, in order to effectively reduce production costs and develop emerging markets, automobile and parts enterprises began to accelerate industrial transfer to China, India, Southeast Asia and other countries and regions, bringing broad growth space to China's auto parts market. Although there is still a large gap in the design, research and development and production capacity of China's auto parts enterprises compared with the traditional automobile industry powers, with the rapid development of China's automobile industry in recent years, the design, research and development and production capacity of domestic parts and components enterprises have made great progress, and have gradually been recognized by many main engine factories.

At the same time, in order to meet the needs of Chinese consumers and reduce procurement costs, joint venture manufacturers choose more domestic-funded auto parts enterprises with increasing R&D capabilities and process levels, thus bringing opportunities for China's auto parts enterprises to replace the original high-cost foreign-funded parts enterprises.

04The auto parts industry is developing in the direction of energy conservation, emission reduction and new energy

Under the trend of global energy conservation and environmental protection, the automobile and auto parts industry has gradually shown the development trend of energy conservation, emission reduction and new energy. In the field of automobile energy conservation and emission reduction, on the one hand, the main engine factory improves the engine, gearbox and optimizes the body aerodynamic structure to improve the combustion efficiency of the engine, reduce fuel consumption, and reduce the emission of pollutants during the driving process. On the other hand, we will promote the development of lightweight automobiles, reduce fuel consumption and reduce carbon emissions by reducing the weight of the body. Relevant data show that for every 10% reduction in the weight of the car, fuel consumption can be reduced by 6%-8%, so reducing the weight of the car and auto parts is one of the important measures for energy conservation and emission reduction. Specifically, the current mainstream ways to reduce the body's self-weight include replacing mainstream steel parts with parts made of plastic, aluminum alloy and other materials, and reducing the self-weight by optimizing the overall layout of the body.

New energy vehicles refer to the use of unconventional vehicle fuels as a power source, comprehensive advanced technology in the power control and drive of vehicles, and the formation of advanced technical principles, new technologies and new structures, mainly including hybrid electric vehicles, pure electric vehicles, fuel cell electric vehicles, other new energy vehicles, etc. Under the pressure of energy and environmental protection, new energy vehicles will become the development direction of future automobiles. With the introduction of various national support policies for new energy vehicles, China's new energy vehicle industry has developed strongly in recent years. According to data from the China Association of Automobile Manufacturers, China's new energy vehicle production and sales volume will be 2021.354 million units in 49, with sales of 352.05 million units, a year-on-year increase of 159.48% and 157.48% respectively. With the increase of the penetration rate of new energy vehicles, the proportion of new energy vehicle parts products in the auto parts market will be further increased, and parts companies that can occupy the first-mover advantage in the field of new energy supporting products will get greater development space, so auto parts companies show a trend of new energy development.

05Enterprises with core technology and good resource integration capabilities will be more competitive

In China's auto parts competition pattern, auto parts companies mainly around the dominant OEM in the automotive industry to carry out business, only through the OEM strict certification process, parts enterprises are eligible to become qualified suppliers of OEM. At present, through continuous scientific and technological innovation, some domestic-funded auto parts enterprises have formed core technologies with independent intellectual property rights, enhanced their market competitiveness, and realized domestic substitution of imports in some core parts and components dominated by foreign-funded enterprises. In the future, with the further intensification of competition in the automobile and auto parts industry, OEMs will put forward higher requirements for the research and development capabilities, production processes and product performance of parts enterprises, so auto parts companies with core technologies and good resource integration capabilities will be more competitive.